Attend Pinellas County Extension’s July Classes

Pinellas County Extension offers residents a wide variety of classes to help them make sustainable decisions.

Be sure to check out our lunch break online classes in July, “Solutions in 30.” Each week this month there will be a special topic presented on Wednesdays at 12:15 pm in the form of a webinar. Take your choice of any of these free webinars: Home Buying Basics, Understanding Your Power Bill, Green Jobs, and Vegetable Garden Problems.

Solutions in 30:

July 7, 2010 - Home Buying Basics

July 14, 2010 - Understanding Your Power Bill

July 21, 2010 - Green Jobs

July 28, 2010 - Vegetable Garden Problems

Families and Consumers:

July 13, 2010 - Focus on Finances

Commercial (Pesticide/FNGLA/ISA) CEUs:

July 7, 2010 - Best Management Practices

July 20, 2010 - Roundup License Training – LCLM

Lawn & Garden:

July 10, 2010 - Rain Harvesting Workshop

July 14, 2010 - http://pinellas.obsres.com/botanical/Info.aspx?EventID=3004

Ju14, 2010 - http://pinellas.obsres.com/botanical/Info.aspx?EventID=3004

July 17, 2010 - Preparing Your Fall Vegetable Garden

July 24, 2010 - Planting, Setting and Growing

July 27 17, 2010 - Using Worms in the Garden

July 31, 2010 - Pests and Harvesting

Urban Wildlife:

July 10, 2010 - Florida Snakes

Sustainable Living:

July 8, 2010 - GreenStar BASICS – Waste Reduction

July15, 2010 - GreenStar BASICS – Green Purchasing

July 17, 2010 - Pinellas Energy Efficiency Project

July 22, 2010 - GreenStar BASICS – Chemical Reduction

July 29, 2010 - GreenStar BASICS – Energy Efficiency

4-H Youth Development:

July 10, 2010 - College 101: New College Student’s Success

You can register for classes online at http://www.pinellascountyextension.org/

Please look for and click on the “Online Class Registration” button on the right hand side near the top of the page

June 30, 2010

June 24, 2010

When Thunder Roars, Go Indoors!

The week of June 20-26 has been designated by NOAA's National Weather Service as Lightning Safety Awareness Week. Lightning has special significance in Florida, since our state leads the nation in lightning strikes. To date since 1959, 98 people have been killed by lightning in the three-county area of Miami-Dade, Broward and Palm Beach. This is the greatest total number of lightning deaths of any three contiguous counties in the United States. The long term yearly averages for lightning casualties in the south Florida mainland are two deaths and nine injuries. Lightning is a threat year-round in south Florida, and lightning casualties have been noted in every month except January. Sadly, the vast majority of these lightning casualties could have been prevented had preventive actions been taken. Perhaps the greatest lightning myth is that if it is not raining, lightning can't strike. Lightning has been known to strike up to 10 miles or more away from the main thunderstorm core, and frequently occurs within 5 miles of the thunderstorm core.

The week of June 20-26 has been designated by NOAA's National Weather Service as Lightning Safety Awareness Week. Lightning has special significance in Florida, since our state leads the nation in lightning strikes. To date since 1959, 98 people have been killed by lightning in the three-county area of Miami-Dade, Broward and Palm Beach. This is the greatest total number of lightning deaths of any three contiguous counties in the United States. The long term yearly averages for lightning casualties in the south Florida mainland are two deaths and nine injuries. Lightning is a threat year-round in south Florida, and lightning casualties have been noted in every month except January. Sadly, the vast majority of these lightning casualties could have been prevented had preventive actions been taken. Perhaps the greatest lightning myth is that if it is not raining, lightning can't strike. Lightning has been known to strike up to 10 miles or more away from the main thunderstorm core, and frequently occurs within 5 miles of the thunderstorm core. The key to remaining safe from this type of lightning strike is to keep an eye to the sky and watch for darkening skies on the horizon along with distant rumbles of thunder. Don't just look overhead for signs of an approaching storm! The main thing to remember regarding lightning safety is: being outside is never safe during a thunderstorm! This includes park pavilions, picnic shelters and baseball dugouts which provide a false sense of safety since they are covered. Bodies of water and trees are also very dangerous places to be during a thunderstorm. Get to a safe shelter immediately if you hear thunder. Remain in

A safe shelter for 30 minutes after the last clap of thunder. Do not be fooled by sunshine or blue sky.

Know the weather forecast before you head outdoors, especially if you are responsible for the safety of others. A portable NOAA All-Hazards Radio is a great way to monitor the latest forecasts and warnings while outdoors. National Weather Service products such as the Hazardous Weather Outlook and Surf Forecast describe the daily lightning danger in south Florida and can be found on the Miami-South Florida National Weather Service website at weather.gov/southflorida or through NOAA All-Hazards Radio.

For further information go to the following web site:

Labels:

lightning,

outdoor safety

June 21, 2010

Our Oceans – Our Responsibility

6/21/10 |

Ramona Madhosingh-Hector, Regional Specialized Agent, Urban Environmental Sustainability, Pinellas County Extension

As the world celebrated World Oceans Day on June 8th, 2010 and the United States celebrated Capitol Hill Oceans Week (June 8-10), there is a general sentiment that an adaptive and integrated policy approach for ocean resources is needed. Such an approach provides flexibility and offers coordination across and among governmental agencies. Heralded as “new” in the United States, Marine Spatial Planning is being proposed as an innovative policy venture for ocean resources. It’s already widely used in Australia, Europe and to a lesser extent, China.

As the world celebrated World Oceans Day on June 8th, 2010 and the United States celebrated Capitol Hill Oceans Week (June 8-10), there is a general sentiment that an adaptive and integrated policy approach for ocean resources is needed. Such an approach provides flexibility and offers coordination across and among governmental agencies. Heralded as “new” in the United States, Marine Spatial Planning is being proposed as an innovative policy venture for ocean resources. It’s already widely used in Australia, Europe and to a lesser extent, China.

The United Nations Educational, Scientific and Cultural Organization (UNESCO) is an arm of the United Nations that is working towards advancing marine spatial planning. Marine Spatial Planning (MSP) is part of the United Nations’ focus on sustainable development practices throughout the world and is defined as:

How new is the concept of MSP and how different is it from the approaches that we currently use in the United States? MSP is similar to coastal zone management and the United States has been using such an approach since the passing of the Coastal Zone Management Act in 1972. The Florida Keys National Marine Sanctuary , established in 1990, uses a comprehensive management plan which is similar to MSP. The driving force behind that designation was protection of the coral reefs which were being affected by declining water quality, pollution and overfishing - a result of rapid urbanization in the Florida Keys. The comprehensive management plan took 6 years to develop and includes the National Oceanic and Atmospheric Administration (NOAA), the Florida Department of Environmental Protection, and the Florida Fish and Wildlife Conservation Commission as co-trustees of the area. At least 30 public meetings were conducted beginning in 1992 and the final draft plan incorporated 6,400 public comments. Although this approach is time intensive and difficult, it is much more successful because it includes a wide variety of partners and allows public stakeholders to contribute to the process and the resulting plan. This “ownership” reduces user conflicts, establishes authority and identifies boundaries of the protected area. The 5 year timeframe for updating the plan provides the “adaptive” element allowing the users to identify new challenges while acknowledging its successes over the previous timeframe.

Marine Spatial Planning is not the same as the more commonly recognized Marine Protected Areas (MPA) or “marine reserve”. In the U.S., a MPA is “any area of the marine environment that has been reserved by federal, state…to provide lasting protection for part or all of the natural and cultural resources.” A MPA might be the result of a marine spatial plan but its approach does not cover the broad spectrum of ecological, economic, social, and cultural values that MSP does. Benefits of MSP include promotion of efficient use of resources and space, identification of areas of biological or ecological importance, protection of cultural heritage, and improved opportunities for citizen involvement.

In June 2009, one year after the United Nations declaration that June 8th would be recognized as World Oceans Day, the United States White House established an Interagency Ocean Policy Task Force. The task force would work towards a new policy approach that would reduce user conflicts, engage public participation and bring together federal, state and tribal partners recognizing the important role that oceans and coasts play in “energy resources, …economy, and trade, …[and] global mobility” while underscoring the “stewardship responsibility to maintain healthy, resilient, and sustainable oceans, [and] coasts.”

The NOAA, a partner in the Ocean Policy Task Force, refers to MSP as “coastal and marine spatial planning” and recognizes that it is a rapidly evolving and dynamic topic area that requires strong partnerships. According to NOAA, effective coastal and marine spatial planning must follow three basic principles and a number of coordinated steps.

As our nation grapples with an immediate ocean disaster in the Gulf of Mexico, Marine Spatial Planning presents a comprehensive but adaptive approach to balance human needs and resource protection. As individuals, we can assist in the preparation of such plans by participating in the “public” elements that collect data from affected and interested citizens and constituents.

Resource Links:

EPA’s Integrated Management of Ocean Resources

Integrated Ocean Observing System

Coastal and Marine Spatial Planning in Practice

Intergovernmental Oceanographic Commission

Marine Spatial Planning FAQs

UNESCO Marine Spatial Planning References

Ramona Madhosingh-Hector, Regional Specialized Agent, Urban Environmental Sustainability, Pinellas County Extension

The United Nations Educational, Scientific and Cultural Organization (UNESCO) is an arm of the United Nations that is working towards advancing marine spatial planning. Marine Spatial Planning (MSP) is part of the United Nations’ focus on sustainable development practices throughout the world and is defined as:

• ecosystem-based - balances ecological, economic, and social goals and objectives toward sustainable development; andIs there a need for marine spatial planning? Indeed there is - marine resources are “common property resources” with open and free access to users. As with most things that are free and unregulated, there is excessive use resulting in decline and sometimes loss of the resource. Already, our marine resources are being threatened by overfishing, pollution and species loss e.g. corals.

• integrated – involves economic sectors and governmental agencies; and

• participatory – actively involves stakeholders

How new is the concept of MSP and how different is it from the approaches that we currently use in the United States? MSP is similar to coastal zone management and the United States has been using such an approach since the passing of the Coastal Zone Management Act in 1972. The Florida Keys National Marine Sanctuary , established in 1990, uses a comprehensive management plan which is similar to MSP. The driving force behind that designation was protection of the coral reefs which were being affected by declining water quality, pollution and overfishing - a result of rapid urbanization in the Florida Keys. The comprehensive management plan took 6 years to develop and includes the National Oceanic and Atmospheric Administration (NOAA), the Florida Department of Environmental Protection, and the Florida Fish and Wildlife Conservation Commission as co-trustees of the area. At least 30 public meetings were conducted beginning in 1992 and the final draft plan incorporated 6,400 public comments. Although this approach is time intensive and difficult, it is much more successful because it includes a wide variety of partners and allows public stakeholders to contribute to the process and the resulting plan. This “ownership” reduces user conflicts, establishes authority and identifies boundaries of the protected area. The 5 year timeframe for updating the plan provides the “adaptive” element allowing the users to identify new challenges while acknowledging its successes over the previous timeframe.

Marine Spatial Planning is not the same as the more commonly recognized Marine Protected Areas (MPA) or “marine reserve”. In the U.S., a MPA is “any area of the marine environment that has been reserved by federal, state…to provide lasting protection for part or all of the natural and cultural resources.” A MPA might be the result of a marine spatial plan but its approach does not cover the broad spectrum of ecological, economic, social, and cultural values that MSP does. Benefits of MSP include promotion of efficient use of resources and space, identification of areas of biological or ecological importance, protection of cultural heritage, and improved opportunities for citizen involvement.

In June 2009, one year after the United Nations declaration that June 8th would be recognized as World Oceans Day, the United States White House established an Interagency Ocean Policy Task Force. The task force would work towards a new policy approach that would reduce user conflicts, engage public participation and bring together federal, state and tribal partners recognizing the important role that oceans and coasts play in “energy resources, …economy, and trade, …[and] global mobility” while underscoring the “stewardship responsibility to maintain healthy, resilient, and sustainable oceans, [and] coasts.”

The NOAA, a partner in the Ocean Policy Task Force, refers to MSP as “coastal and marine spatial planning” and recognizes that it is a rapidly evolving and dynamic topic area that requires strong partnerships. According to NOAA, effective coastal and marine spatial planning must follow three basic principles and a number of coordinated steps.

As our nation grapples with an immediate ocean disaster in the Gulf of Mexico, Marine Spatial Planning presents a comprehensive but adaptive approach to balance human needs and resource protection. As individuals, we can assist in the preparation of such plans by participating in the “public” elements that collect data from affected and interested citizens and constituents.

Resource Links:

EPA’s Integrated Management of Ocean Resources

Integrated Ocean Observing System

Coastal and Marine Spatial Planning in Practice

Intergovernmental Oceanographic Commission

Marine Spatial Planning FAQs

UNESCO Marine Spatial Planning References

Labels:

coastal,

Marine,

sustainability

June 15, 2010

Are You Ready For Retirement?

6/15/10 |

Karen Saley, Extension Specialist, Pinellas County Extension

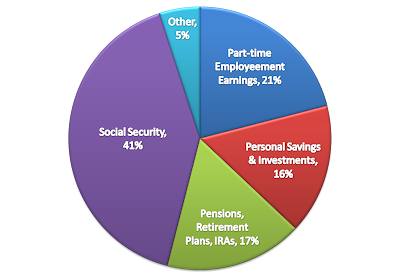

Retirement can either be a pleasure or a struggle depending on how well you did your planning. During our retirement years our income shifts from salary and wages to social security, personal savings, retirement plans and for many, part-time employment. Unfortunately, many of us thought we could rely on social security as the main source of income in retirement. Sad to say, this is not the case. According to the latest figures only 41 percent of our income will come from social security. That means more than 50 percent of our retirement income must come from other sources if we would like to continue to live our current lifestyle.

Retirement planning tips

Employer-sponsored retirement plan

Join us for a live webinar on June 23, 2010 at 12:15pm when we will discuss in more detail employer-sponsored and personally established retirement accounts. http://pinellas.ifas.ufl.edu/

Karen Saley, Extension Specialist, Pinellas County Extension

Retirement can either be a pleasure or a struggle depending on how well you did your planning. During our retirement years our income shifts from salary and wages to social security, personal savings, retirement plans and for many, part-time employment. Unfortunately, many of us thought we could rely on social security as the main source of income in retirement. Sad to say, this is not the case. According to the latest figures only 41 percent of our income will come from social security. That means more than 50 percent of our retirement income must come from other sources if we would like to continue to live our current lifestyle.

Retirement planning tips

- Start saving early and regularly by investing in mutual funds through tax-sheltered retirement accounts.

- Establish a diversified investment portfolio.

- Take advantage of an employer-sponsored retirement plan by contributing at least the amount required to obtain the full matching contribution from your employer.

- Contribute to Roth IRA and/or traditional IRA accounts.

- When changing employers, roll over the funds into the new employer’s plan or a rollover IRA.

- Don’t touch your retirement savings for any reason.

Employer-sponsored retirement plan

- Defined-contribution

- 401(k) private corporations

- 403(b) colleges, hospitals, religious organizations and other nonprofits

- 457 plans state and local governments

- Defined-benefit

- Pension: Sum of money of money paid regularly by a former employer as a retirement benefit.

- Cash-balance : Interest-earning account credited with a percentage of pay on a monthly basis. Only the employer contributes to the plan.

- Employee stock-ownership plan (ESOP): Benefit plan in which employers make tax-deductible gifts of company stock into trusts which are then allocated into employee accounts.

- Profit-sharing plan: Employer sponsored plan that allocates some of the employer profits to employees in the form of end-of-the year cash or common stock contributions to employee’s 401 (k) accounts.

- Individual retirement account (IRA): Personal retirement account which a person can make annual contributions that provide tax-deferred growth.

- Traditional IRA – Account that offers tax-deferred growth; the initial contribution may be tax deductible for the year that the IRA was funded.

- Roth IRA – IRA funded with after-tax money (and thus is not tax deductable) that grows on a tax-deferred basis; withdrawals are not subject to taxation

- Keoghs: A tax-deferred retirement account designed for self-employed and small-business owners.

- Simplified employee pension-individual retirement account (SEP-IRA): Intended for taxpayers with self-employment income and owners of small businesses.

Join us for a live webinar on June 23, 2010 at 12:15pm when we will discuss in more detail employer-sponsored and personally established retirement accounts. http://pinellas.ifas.ufl.edu/

Labels:

Money,

retirement

June 10, 2010

News Release - Exercise Caution when Making Legal Decisions Related to Damages from the Deepwater Horizon Oil Spill

University of Florida

Florida Sea Grant College Program

For Immediate Release:

Exercise Caution when Making Legal Decisions

Related to Damages from the Deepwater Horizon Oil Spill

An Advisory Compiled by Thomas Ruppert, Esq.

Coastal Planning Specialist, Florida Sea Grant College Program

(Gainesville, Fla.) – Since the explosion on the Deepwater Horizon oil rig, Gulf Coast residents have been the targets of aggressive advertising campaigns by law firms seeking clients for litigation related to the oil spill.

Although Gulf Coast residents are entitled to compensation from BP and other responsible parties for certain losses, claimants should exercise caution to ensure initial actions do not affect future legal rights. You do not need to be in a hurry, because by law you have at least three years to file a claim. Taking time to weigh options carefully before acting will not result in lost legal rights. Acting hastily could limit your ability to secure temporary financial assistance.

Things every Florida resident should know

1) Anyone who has suffered damages to property or business due to the oil spill may seek compensation directly from BP.

You may do this without the assistance of a lawyer by calling BP’s claims line at 1-800-440-0858, or by visiting a local BP claims office in your area, if available. Florida residents may apply at the online claims submission page from BP’s Florida Gulf Response Web site at http://www.floridagulfresponse.com/.

2) Participating in any lawsuit against BP, such as a class-action suit, will likely prevent you from receiving immediate or short-term compensation.

Some claimants are already receiving short-term compensation from BP, but BP is unlikely to consider your claim if you are a part of a lawsuit against them. It should also be noted that accepting payment now does not prevent you from receiving temporary or short-term compensation from BP in the future.

3) There is a federal backup to the BP claims process.

BP has 90 days to respond to your claim, but if it fails to process your claim in that time or denies it, you have a right to seek payment from the Oil Spill Liability Trust Fund. Claims must be submitted to the Coast Guard’s National Pollution Funds Center (NPFC) (http://www.uscg.mil/npfc/Claims/default.asp).

You have three years from the date of the incident to file a claim with the federal Trust Fund. If you accept money, you cannot later file a lawsuit against any party to recover costs or damages which were the subject of the compensated claim. If payment is received from another source, such as insurance, you must reimburse the Fund. Currently there is a $1-billion cap on expenditures from the trust fund per incident. The Funds Center processes claims in the order they are received.

4) If you choose to sue BP instead of using BP’s claims process, Florida law gives you four years, not just three, from the date of the harm to file suit.

Use this time to compile your records, document losses, and learn more about your situation and your legal rights. Be certain to preserve all possible evidence of your damages, including photos, financial records, cancellations, or any other evidence of loss of work or income as well as activities you take to minimize your losses.

5) There are rules that govern how lawyers may solicit you for your business.

Generally, a lawyer, or lawyer’s representative, may not contact you to solicit employment in person or by telephone, unless you have previously contacted the law firm.

The rules vary, however, for written communication. Attorneys may send you an unsolicited email or letter if two conditions are met. First, the material must disclose one or more actual office locations of the lawyer who will perform the services advertised. Second, it must clearly be marked as an advertisement. For an email, this means the subject line must begin “legal advertisement.” Printed material must bear the word “advertisement” in red ink.

Attorneys may advertise on television and radio, but only attorneys licensed in Florida may file lawsuits in Florida.

If you believe you have been improperly solicited by a lawyer, you should report it immediately by contacting the Attorney/Consumer Assistance Program (ACAP) at 1-866-352-0707.

6) Once you retain a lawyer, BP is not permitted to contact you directly.

BP is required to only communicate with your attorney unless your attorney, in writing, authorizes BP to communicate directly with you.

7) Carefully read all accompanying documents before you accept payment from BP for a damage claim.

If you have applied for immediate damages from BP, you need not turn down any offer of money, but if the forms you sign when you receive the money contain language releasing BP from any further liability, this may prevent you from seeking future compensation.

If you are asked to sign anything you do not fully and clearly understand, you should consult your own attorney. Your attorney should review all documents prior to signing to ensure you are not giving up future rights in return for what you view as only partial payment for all the claims you may eventually have.

Some attorneys advise writing “with reservations” just above where you countersign the check, especially if you accept a check without signing any other papers and you do not view the payment as full payment for all your damages. It could help in your claim should BP assert that you accepted the check as complete payment. You should also keep a copy of both sides of the signed check for your records.

8) If you need immediate legal advice, seek attorney referrals from trusted individuals.

Optionally, the Florida Bar Lawyer Referral Service offers referral for a slight charge. That number is 1-800-342-8011. You can also check the Florida Bar Association’s attorney online directory, http://www.floridabar.org/. Select “Public Information” on the left tool bar and then choose “Find a Lawyer”.

9) Don’t be influenced by stories you hear about the Exxon Valdez oil spill.

You may hear a lot about the $2.5 billion in damages a jury awarded to injured parties following the Exxon Valdez spill. That verdict, however, did not stand, for reasons that extend beyond the scope of this advisory, and was reduced to $507.5 million. While this may sound large, Exxon did not begin writing compensation checks until November 2009, some 20 years after the original spill. Some of the plaintiffs received less than $100 in punitive damages.

The key point is that any award you might receive from a lawsuit would likely not come for many years, could be very small, and would almost certainly prevent you from receiving short-term compensation for your actual damages.

Contact: Heather Hammers, Florida Sea Grant Extension Agent, Pinellas County hhammers@pinellascounty.org (727) 582-2658

Florida Sea Grant College Program

Building 803 McCarty Drive

PO Box 110400

Gainesville, FL 32611-0400

(352) 392-5870

FAX (352) 392-5113

http://www.flseagrant.org/

June 8, 2010 PO Box 110400

Gainesville, FL 32611-0400

(352) 392-5870

FAX (352) 392-5113

http://www.flseagrant.org/

For Immediate Release:

Exercise Caution when Making Legal Decisions

Related to Damages from the Deepwater Horizon Oil Spill

An Advisory Compiled by Thomas Ruppert, Esq.

Coastal Planning Specialist, Florida Sea Grant College Program

(Gainesville, Fla.) – Since the explosion on the Deepwater Horizon oil rig, Gulf Coast residents have been the targets of aggressive advertising campaigns by law firms seeking clients for litigation related to the oil spill.

Although Gulf Coast residents are entitled to compensation from BP and other responsible parties for certain losses, claimants should exercise caution to ensure initial actions do not affect future legal rights. You do not need to be in a hurry, because by law you have at least three years to file a claim. Taking time to weigh options carefully before acting will not result in lost legal rights. Acting hastily could limit your ability to secure temporary financial assistance.

Things every Florida resident should know

1) Anyone who has suffered damages to property or business due to the oil spill may seek compensation directly from BP.

You may do this without the assistance of a lawyer by calling BP’s claims line at 1-800-440-0858, or by visiting a local BP claims office in your area, if available. Florida residents may apply at the online claims submission page from BP’s Florida Gulf Response Web site at http://www.floridagulfresponse.com/.

2) Participating in any lawsuit against BP, such as a class-action suit, will likely prevent you from receiving immediate or short-term compensation.

Some claimants are already receiving short-term compensation from BP, but BP is unlikely to consider your claim if you are a part of a lawsuit against them. It should also be noted that accepting payment now does not prevent you from receiving temporary or short-term compensation from BP in the future.

3) There is a federal backup to the BP claims process.

BP has 90 days to respond to your claim, but if it fails to process your claim in that time or denies it, you have a right to seek payment from the Oil Spill Liability Trust Fund. Claims must be submitted to the Coast Guard’s National Pollution Funds Center (NPFC) (http://www.uscg.mil/npfc/Claims/default.asp).

You have three years from the date of the incident to file a claim with the federal Trust Fund. If you accept money, you cannot later file a lawsuit against any party to recover costs or damages which were the subject of the compensated claim. If payment is received from another source, such as insurance, you must reimburse the Fund. Currently there is a $1-billion cap on expenditures from the trust fund per incident. The Funds Center processes claims in the order they are received.

4) If you choose to sue BP instead of using BP’s claims process, Florida law gives you four years, not just three, from the date of the harm to file suit.

Use this time to compile your records, document losses, and learn more about your situation and your legal rights. Be certain to preserve all possible evidence of your damages, including photos, financial records, cancellations, or any other evidence of loss of work or income as well as activities you take to minimize your losses.

5) There are rules that govern how lawyers may solicit you for your business.

Generally, a lawyer, or lawyer’s representative, may not contact you to solicit employment in person or by telephone, unless you have previously contacted the law firm.

The rules vary, however, for written communication. Attorneys may send you an unsolicited email or letter if two conditions are met. First, the material must disclose one or more actual office locations of the lawyer who will perform the services advertised. Second, it must clearly be marked as an advertisement. For an email, this means the subject line must begin “legal advertisement.” Printed material must bear the word “advertisement” in red ink.

Attorneys may advertise on television and radio, but only attorneys licensed in Florida may file lawsuits in Florida.

If you believe you have been improperly solicited by a lawyer, you should report it immediately by contacting the Attorney/Consumer Assistance Program (ACAP) at 1-866-352-0707.

6) Once you retain a lawyer, BP is not permitted to contact you directly.

BP is required to only communicate with your attorney unless your attorney, in writing, authorizes BP to communicate directly with you.

7) Carefully read all accompanying documents before you accept payment from BP for a damage claim.

If you have applied for immediate damages from BP, you need not turn down any offer of money, but if the forms you sign when you receive the money contain language releasing BP from any further liability, this may prevent you from seeking future compensation.

If you are asked to sign anything you do not fully and clearly understand, you should consult your own attorney. Your attorney should review all documents prior to signing to ensure you are not giving up future rights in return for what you view as only partial payment for all the claims you may eventually have.

Some attorneys advise writing “with reservations” just above where you countersign the check, especially if you accept a check without signing any other papers and you do not view the payment as full payment for all your damages. It could help in your claim should BP assert that you accepted the check as complete payment. You should also keep a copy of both sides of the signed check for your records.

8) If you need immediate legal advice, seek attorney referrals from trusted individuals.

Optionally, the Florida Bar Lawyer Referral Service offers referral for a slight charge. That number is 1-800-342-8011. You can also check the Florida Bar Association’s attorney online directory, http://www.floridabar.org/. Select “Public Information” on the left tool bar and then choose “Find a Lawyer”.

9) Don’t be influenced by stories you hear about the Exxon Valdez oil spill.

You may hear a lot about the $2.5 billion in damages a jury awarded to injured parties following the Exxon Valdez spill. That verdict, however, did not stand, for reasons that extend beyond the scope of this advisory, and was reduced to $507.5 million. While this may sound large, Exxon did not begin writing compensation checks until November 2009, some 20 years after the original spill. Some of the plaintiffs received less than $100 in punitive damages.

The key point is that any award you might receive from a lawsuit would likely not come for many years, could be very small, and would almost certainly prevent you from receiving short-term compensation for your actual damages.

Florida Sea Grant provides this non-advocacy legal research

as a public service to Florida citizens.

-30-

Contact: Heather Hammers, Florida Sea Grant Extension Agent, Pinellas County hhammers@pinellascounty.org (727) 582-2658

Labels:

Florida Sea Grant,

Marine,

oil spill

Subscribe to:

Posts (Atom)